本文共 5587 字,大约阅读时间需要 18 分钟。

内容概要

- 如何使用pandas读入数据

- 如何使用seaborn进行数据的可视化

- scikit-learn的线性回归模型和使用方法

- 线性回归模型的评估测度

- 特征选择的方法

作为有监督学习,分类问题是预测类别结果,而回归问题是预测一个连续的结果。

1. 使用pandas来读取数据

Pandas是一个用于数据探索、数据处理、数据分析的库

import pandas as pd # read csv file directly from a URL and save the resultsdata = pd.read_csv('http://www-bcf.usc.edu/~gareth/ISL/Advertising.csv', index_col=0)# display the first 5 rowsdata.head() 上面显示的结果类似一个电子表格,这个结构称为Pandas的数据帧(data frame)。

pandas的两个主要:Series和DataFrame:

- Series类似于一维数组,它有一组数据以及一组与之相关的数据标签(即索引)组成。

- DataFrame是一个表格型的数据结构,它含有一组有序的列,每列可以是不同的值类型。DataFrame既有行索引也有列索引,它可以被看做由Series组成的字典。

# display the last 5 rowsdata.tail() # check the shape of the DataFrame(rows, colums)data.shape 特征:

- TV:对于一个给定市场中单一产品,用于电视上的广告费用(以千为单位)

- Radio:在广播媒体上投资的广告费用

- Newspaper:用于报纸媒体的广告费用

响应:

- Sales:对应产品的销量

在这个案例中,我们通过不同的广告投入,预测产品销量。因为响应变量是一个连续的值,所以这个问题是一个回归问题。数据集一共有200个观测值,每一组观测对应一个市场的情况。

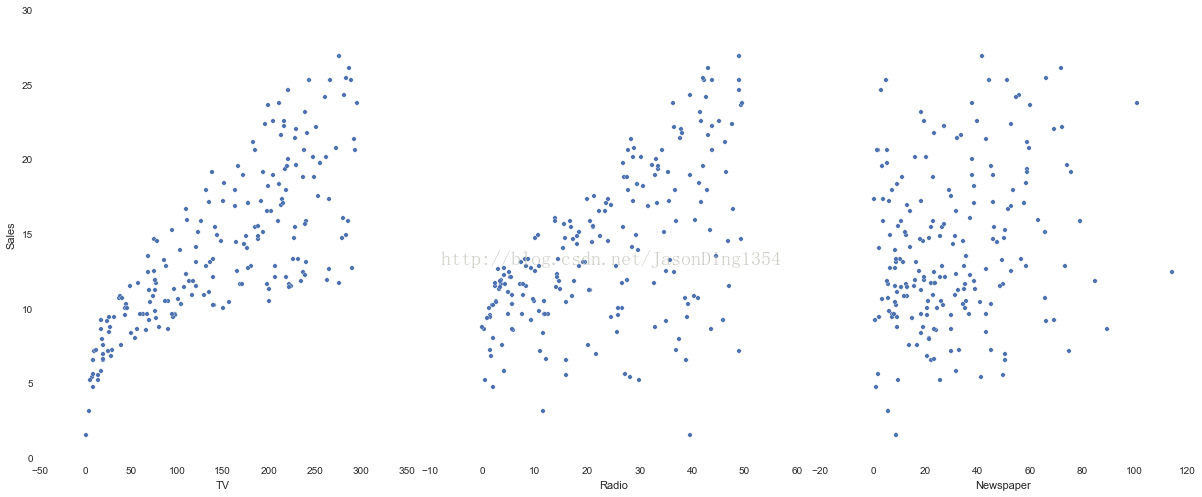

import seaborn as sns%matplotlib inline # visualize the relationship between the features and the response using scatterplotssns.pairplot(data, x_vars=['TV','Radio','Newspaper'], y_vars='Sales', size=7, aspect=0.8)

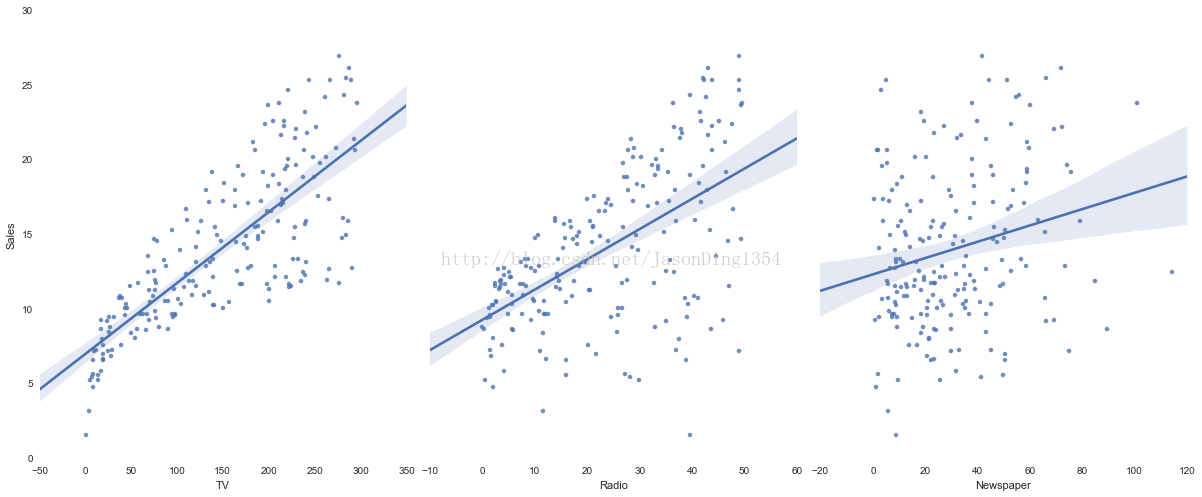

seaborn的pairplot函数绘制X的每一维度和对应Y的散点图。通过设置size和aspect参数来调节显示的大小和比例。可以从图中看出,TV特征和销量是有比较强的线性关系的,而Radio和Sales线性关系弱一些,Newspaper和Sales线性关系更弱。通过加入一个参数kind='reg',seaborn可以添加一条最佳拟合直线和95%的置信带。

sns.pairplot(data, x_vars=['TV','Radio','Newspaper'], y_vars='Sales', size=7, aspect=0.8, kind='reg')

2. 线性回归模型

优点:快速;没有调节参数;可轻易解释;可理解

缺点:相比其他复杂一些的模型,其预测准确率不是太高,因为它假设特征和响应之间存在确定的线性关系,这种假设对于非线性的关系,线性回归模型显然不能很好的对这种数据建模。

线性模型表达式: y=β0+β1x1+β2x2+...+βnxn 其中

- y是响应

- β0是截距

- β1是x1的系数,以此类推

在这个案例中: y=β0+β1∗TV+β2∗Radio+...+βn∗Newspaper

(1)使用pandas来构建X和y

- scikit-learn要求X是一个特征矩阵,y是一个NumPy向量

- pandas构建在NumPy之上

- 因此,X可以是pandas的DataFrame,y可以是pandas的Series,scikit-learn可以理解这种结构

# create a python list of feature namesfeature_cols = ['TV', 'Radio', 'Newspaper']# use the list to select a subset of the original DataFrameX = data[feature_cols]# equivalent command to do this in one lineX = data[['TV', 'Radio', 'Newspaper']]# print the first 5 rowsX.head() # check the type and shape of Xprint type(X)print X.shape # select a Series from the DataFramey = data['Sales']# equivalent command that works if there are no spaces in the column namey = data.Sales# print the first 5 valuesy.head() print type(y)print y.shape (2)构造训练集和测试集

from sklearn.cross_validation import train_test_splitX_train, X_test, y_train, y_test = train_test_split(X, y, random_state=1) # default split is 75% for training and 25% for testingprint X_train.shapeprint y_train.shapeprint X_test.shapeprint y_test.shape (3)Scikit-learn的线性回归

from sklearn.linear_model import LinearRegressionlinreg = LinearRegression()linreg.fit(X_train, y_train) print linreg.intercept_print linreg.coef_ # pair the feature names with the coefficientszip(feature_cols, linreg.coef_) y=2.88+0.0466∗TV+0.179∗Radio+0.00345∗Newspaper

如何解释各个特征对应的系数的意义?

- 对于给定了Radio和Newspaper的广告投入,如果在TV广告上每多投入1个单位,对应销量将增加0.0466个单位

- 更明确一点,加入其它两个媒体投入固定,在TV广告上没增加1000美元(因为单位是1000美元),销量将增加46.6(因为单位是1000)

(4)预测

y_pred = linreg.predict(X_test) 3. 回归问题的评价测度

对于分类问题,评价测度是准确率,但这种方法不适用于回归问题。我们使用针对连续数值的评价测度(evaluation metrics)。

下面介绍三种常用的针对回归问题的评价测度

# define true and predicted response valuestrue = [100, 50, 30, 20]pred = [90, 50, 50, 30] (1)平均绝对误差(Mean Absolute Error, MAE)

1n∑ni=1|yi−yi^|

(2)均方误差(Mean Squared Error, MSE)

1n∑ni=1(yi−yi^)2

(3)均方根误差(Root Mean Squared Error, RMSE)

1n∑ni=1(yi−yi^)2−−−−−−−−−−−−−√

from sklearn import metricsimport numpy as np# calculate MAE by handprint "MAE by hand:",(10 + 0 + 20 + 10)/4.# calculate MAE using scikit-learnprint "MAE:",metrics.mean_absolute_error(true, pred)# calculate MSE by handprint "MSE by hand:",(10**2 + 0**2 + 20**2 + 10**2)/4.# calculate MSE using scikit-learnprint "MSE:",metrics.mean_squared_error(true, pred)# calculate RMSE by handprint "RMSE by hand:",np.sqrt((10**2 + 0**2 + 20**2 + 10**2)/4.)# calculate RMSE using scikit-learnprint "RMSE:",np.sqrt(metrics.mean_squared_error(true, pred)) 计算Sales预测的RMSE

print np.sqrt(metrics.mean_squared_error(y_test, y_pred)) 4. 特征选择

在之前展示的数据中,我们看到Newspaper和销量之间的线性关系比较弱,现在我们移除这个特征,看看线性回归预测的结果的RMSE如何?

feature_cols = ['TV', 'Radio']X = data[feature_cols]y = data.SalesX_train, X_test, y_train, y_test = train_test_split(X, y, random_state=1)linreg.fit(X_train, y_train)y_pred = linreg.predict(X_test)print np.sqrt(metrics.mean_squared_error(y_test, y_pred)) 我们将Newspaper这个特征移除之后,得到RMSE变小了,说明Newspaper特征不适合作为预测销量的特征,于是,我们得到了新的模型。我们还可以通过不同的特征组合得到新的模型,看看最终的误差是如何的。